Context Analytics is the leader in processing and structuring textual data for sentiment analysis....

In the evolving world of sentiment analysis, Context Analytics (CA) stands as a leader in processing and structuring textual data from a wide array of sources, including Twitter, StockTwits, Reddit, News, Corporate Filings, and custom inputs. Today, we delve into CA’s Twitter S-Factor feed, a product that grades sentiment from Twitter messages on a scale from -1.000 to 1.000, aggregates them over a 24-hour period, and compares this data to a historical 20-day baseline to create S-Factors. This analysis will focus on how variations in Twitter message volume affect the S-Score metric, shedding light on whether increased volume helps, hurts, or has no effect on sentiment score signals.

Understanding the S-Factor Feed and S-Score

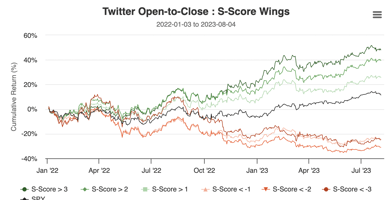

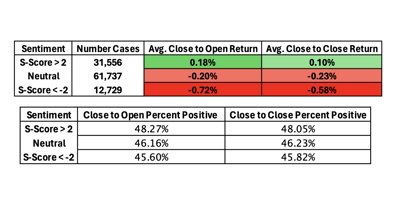

The S-Factor feed is one of CA’s flagship products, providing insights into social sentiment by evaluating how positive or negative the sentiment is for a specific security. The S-Score, calculated by security, offers a cross-sectional view of social sentiment, effectively neutralizing bias towards message volume by comparing the security’s sentiment against its historical baseline. Extensive research has demonstrated the predictive nature of this metric.

Incorporating the SV-Score: Twitter Volume Score

The SV-Score represents a standardized Twitter message volume score, indicating the volume of Tweets over the previous 24 hours relative to the company's own historical data. It follows the same distribution model as the S-Score. For this research, we investigate the effect of increasing the SV-Score threshold by 1 standard deviation increments and quantify the impact on the top and bottom quintiles of the S-Score.

Research Methodology

Our approach involves comparing the normal top and bottom quintiles of the S-Score (without any volume filter) with quintiles derived from securities that meet certain SV-Score thresholds. Specifically, we analyze:

- SV-Score > 0: Companies experiencing higher-than-usual Twitter volume.

- SV-Score > 1: Companies experiencing significantly higher Twitter volume.

- SV-Score > 2: Companies experiencing extremely high Twitter volume.

For each threshold portfolio, we split the securities into quintiles based on the S-Score, focusing on the top (most positive sentiment) and bottom (most negative sentiment) quintiles. This segmentation allows us to form groups like Quintile 1 (SV-Score > 0) and Quintile 5 (SV-Score > 0), which are recalculated daily. All sentiment scores are taken 20 minutes prior to market close, with returns calculated from the subsequent close-to-close period. We compound these portfolios daily from the start of 2018, providing a robust 6.5-year dataset for analysis.

Results and Implications

From 2018 onwards, our research reveals a clear impact of the SV-Score on the S-Score quintiles:

- Negative Sentiment Enhancement: As the SV-Score increases, the negative effect of the bottom quintile sentiment is significantly amplified. For instance, the Quintile 1 (SV-Score > 2) group underperforms notably, losing 22% cumulatively, highlighting a strong negative signal when a company has high Twitter volume and extremely negative sentiment. As the SV-Score threshold decreases, Quintile 1’s negative signal diminishes displaying SV-Score effects on extreme negative sentiment.

- Positive Sentiment Enhancement: The effect on the top quintile, while not as pronounced as the bottom quintile, still shows that including a volume threshold enhances the positive sentiment signal. However, this relationship is less monotonic compared to the bottom quintiles as Quintile 5 (SV-Score > 1) outperforms Quintile 5 (SV-Score > 2).

- Year-to-Date Trends: Recent data for the current year indicates a continued monotonic spread and correlation between the SV-Score and the S-Score quintiles, reinforcing the SV-Score’s utility in enhancing our sentiment signal.

- Confounding Variable Potential: By increasing our SV-Score thresholds, we seem to be naturally selecting more extreme sentiment stocks. As the threshold increases, we observe that the average S-Score (Avg. Score in table) also increases or decreases (depending on whether we're looking at the top or bottom quintiles). This suggests that higher SV-Score thresholds tend to select stocks with more extreme sentiment. Additionally, as the SV-Score thresholds increase, the number of securities available decreases, thus why average count of each quintile decreases.

Conclusion

Our findings indicate that the SV-Score can significantly enhance the predictive power of the S-Score. As Twitter relative volume increases, the signals derived from sentiment analysis become more pronounced, especially for extreme negative sentiment signals. This research provides another method to leverage social sentiment data for robust trading signals, offering valuable insights for traders and risk analysts alike.

For more detailed information and to explore our range of products, visit www.contextanalytics-ai.com or click the button below.